Commentary: Greenspan's bailout legacy is Warsh's straitjacket

Published in Op Eds

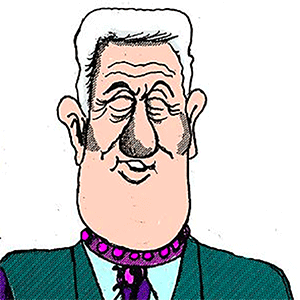

Eulogies tend to laud the departed, not criticize them, so it’s no surprise that the death of Alan Greenspan, the former Federal Reserve Chairman, at age 100 prompted people to say nice things about him.

His passing prompted a tsunami of eulogistic op-eds on how the "maestro" centrally planned the American economy for close to 20 years. But those pieces were conspicuously silent on how Greenspan frequently left the taxpayer with the tab.

His tenure as Chairman kicked off in 1987, when Greenspan used a stock market crash to turn the Fed into a banker’s bailout machine—one where Wall Street keeps the wins but Main Street, and dollar holders broadly, eat the losses.

It became known as the “Greenspan put” (think of a put as insurance in the financial world) and is a big reason why Boomers own everything while Millennials share ramen with roommates at 40. Then came Long Term Capital Management (LTCM), a leveraged hedge fund that collapsed in 1998.

LTCM marked a turning point because it was the first time the Fed formally organized a bailout, creating the ultimate moral hazard that turned into the foundation of “too big to fail.” The mentality continued all the way through 2006, when Greenspan lit the fuse of his last boom-bust bomb, ending in the 2008 Financial Crisis that nearly set off a second Great Depression.

Unfortunately, the bailout machine Greenspan built is now a permanent feature of the Fed, with every subsequent Fed Chairman blowing bubbles, popping them, then bailing out the banks.

It’s a logical cycle for central banks like the Fed since they’re created by bankers as a counterfeiting cartel that prints money for easy profits but not so fast that the inflation makes voters grab the pitchforks. It’s a petty cash thief who’s less likely to get caught than a bank robber.

The main way central banks print money is by letting commercial banks lend money they don't have (they counterfeit the dollars for the loans), then promising to bail out bankers if things go south—the so-called lender of last resort function.

The Fed primarily limits the printing using interest rates to influence how much loans cost. Lower rates mean cheaper loans, which artificially boosts growth, generates more fees for Wall Street, and makes it cheap for the federal government to spend more than it has.

The problem is having an unlimited money printer attracts pressure to cut rates too far and too long, causing inflation. There’s even more insidious pressure from Wall Street to use that lender of last resort function to bail out speculators of bad investments that boomed when rates were artificially low.

It's an iron law of finance that more risk is more return. If you tell gamblers they keep the wins, but you'll cover the losses they'll go all in all the time. That’s what Greenspan helped create starting with Black Monday—the 1987 stock market crash—where he flooded the banking system with money, promising to keep flooding until every banker was solvent.

Bankers went from conservative portly men in three-piece pinstripe suits and glasses to the late 1980s sharks fueled by alcohol and cocaine. Those sharks ultimately fueled 13 financial crises under Greenspan, from the S&L crisis and Tequila crises to the dot-com bubble, the 1994 bond market massacre, the 1997 Asian financial crisis, LTCM, the mother of housing bubbles in the early 2000s, and more.

In every case, the sharks made billions while taxpayers and dollar holders got wrecked. Greenspan oversaw finance quadrupling to become the third-largest industry in America. Worse, it made Wall Street perpetually dependent on the Fed.

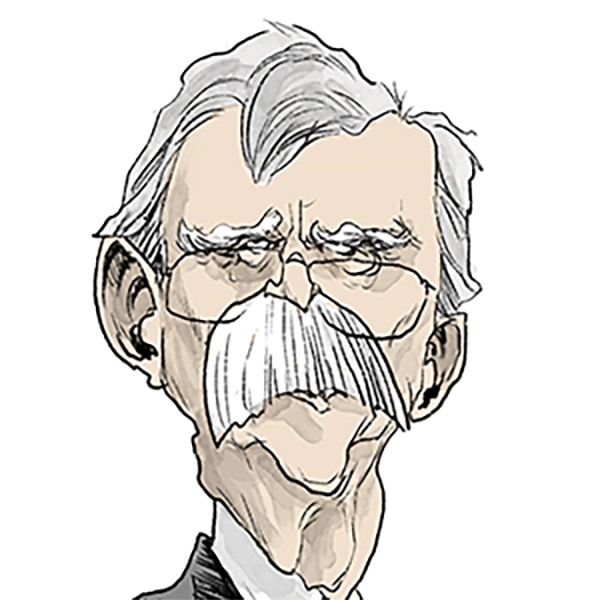

This is why our new Fed Chairman, Kevin Warsh, has an extreme uphill battle in fighting inflation—it requires ending the bailouts on which Wall Street relies. Greenspan may be gone, but the bailout machine he built is still firmly in place. Fixing it is simple: just announce the Fed won't bail anybody out; if a bank fails, it's sold for scrap to more prudent banks.

Of course, that would set off an instant 2008 crisis, meaning it won't happen. The best Warsh can do is increasingly limit the bailouts as time goes on. He’ll need to be a Houdini to get out of the straitjacket Alan Greenspan wove for him.

____

Peter St. Onge, Ph.D., is senior economist and E.J. Antoni, Ph.D., is chief economist at the Heritage Foundation.

_____

©2026 Tribune Content Agency, LLC.

Comments